Does your online revenue growth feel a little exhausted? You are not alone.

Online sales in the Netherlands grew 24% in 2021, followed by a 5.8% decline in 2022. Since then growth has been modest and uneven. The post-COVID tailwind that made top-line growth feel automatic is gone. For many retailers, the conversation has shifted from how to grow revenue to how to protect and improve what is already there.

That shift in focus, from top-line to bottom-line, is not a retreat. It is a strategic adjustment that the best-run retail businesses make deliberately.

Top-line growth versus bottom-line growth

Top-line growth is revenue growth. It comes from acquiring new customers, entering new markets, expanding the product range, or increasing average order value. It is important, and for high-growth businesses it is the primary focus. But it depends on external conditions, consumer confidence, and competitive dynamics that are not always within your control.

Bottom-line growth is different. It is growth in net profit, achieved by improving what happens below the revenue line. Cost reduction, operational efficiency, better supplier terms, smarter allocation of fixed overhead. These levers are largely within your control, and they tend to be more predictable in their impact.

The two are not mutually exclusive. But in a period of slower top-line growth, the bottom-line becomes the more accessible and more certain source of improvement.

Where to look for bottom-line gains

The obvious places include marketing efficiency, where acquisition costs can often be reduced without a proportional drop in revenue, production and fulfilment costs, supplier renegotiation across categories, and overhead optimisation. These are worth reviewing systematically, and most finance teams are already focused on them.

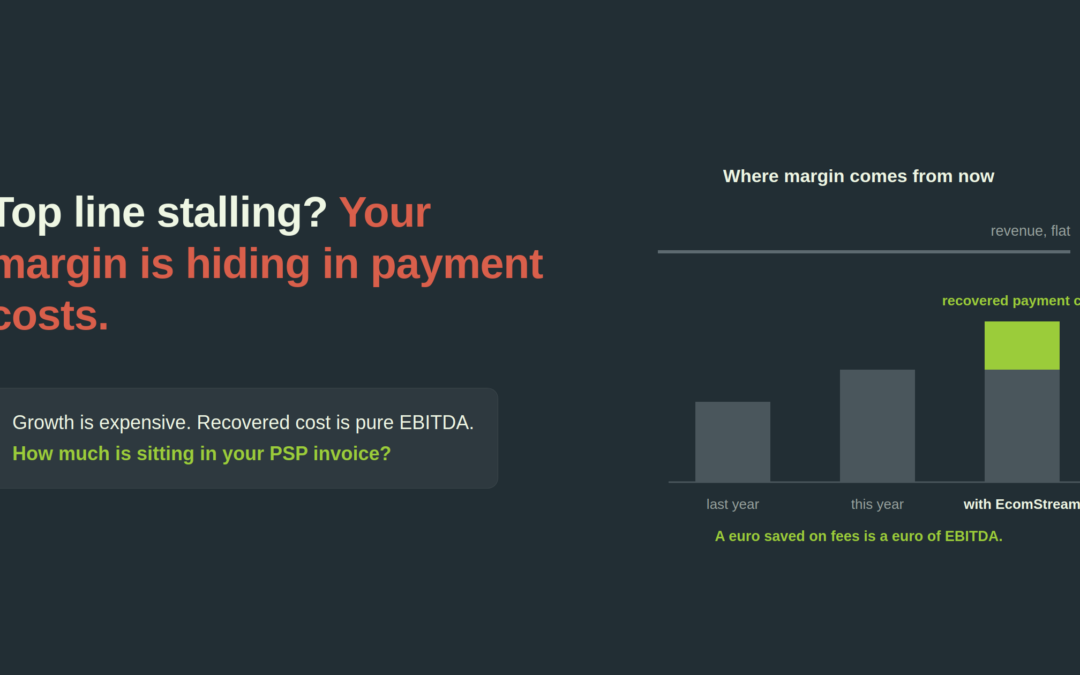

The less obvious place, and for many retailers the most underexploited, is payment processing costs.

Not because payment costs are uniquely large. But because they are uniquely neglected. Most of the obvious cost lines are actively managed. Payment costs rarely are.

Payment costs: the most overlooked bottom-line lever

Payment processing typically represents between 0.5% and 2.5% of revenue for Dutch retailers, depending on the payment method mix, card type split, and current contract terms. For a retailer processing 10 million euros annually, the difference between a well-negotiated payment setup and a default one can easily exceed 100,000 euros per year.

That gap exists because PSP contracts are complex, pricing is opaque, and the internal expertise to scrutinise them is rarely available. PSPs are aware of this. Merchants who do not actively manage their payment costs tend to pay significantly more than those who do.

The good news is that the levers are well understood and the results are measurable.

Interchange optimisation

Not all transactions attract the same interchange rate. The category your transaction falls into depends on how card data is submitted, whether the transaction is authenticated, and what descriptor you send. Misclassification is common and costs money that does not need to be spent. A detailed analysis of your transaction mix typically reveals interchange optimisation opportunities without any need to switch provider.

Scheme fee transparency

The question to ask your PSP is whether scheme fees are passed through at cost or marked up. Moving from blended to interchange-plus pricing gives you genuine visibility into what you are paying and why, and a real basis for negotiating each component independently.

Acquirer margin renegotiation

Your PSP margin is negotiable, particularly if your volumes have grown since your last contract review. Most PSPs have pricing tiers that are not automatically applied, they need to be triggered by a commercial conversation. A formal review process, even if you ultimately stay with your current provider, fundamentally changes the negotiating dynamic.

Local payment method repricing

iDEAL 2.0, Bancontact, and PayPal pricing are all negotiable. Many retailers accept the rates they were quoted at onboarding and never revisit them. For Dutch retailers with high iDEAL volumes in particular, the transition to iDEAL 2.0 has changed the commercial structures, making a review timely.

The case for acting now

Economic headwinds create the conditions for bottom-line focus, but they also create urgency. The retailers who act on cost optimisation during a slower period are the ones who enter the next growth cycle with structurally better margins. Those who wait for revenue growth to return and deal with costs later are making a more expensive choice than it appears.

Payment cost optimisation is particularly well-suited to this moment because the savings are contractual and immediate. Unlike operational efficiency projects that require investment, process change, and time to show results, a renegotiated PSP contract reduces costs from the next invoice cycle.

EcomStream works with Dutch and European retailers on a no-cure-no-pay basis. There is no cost to a diagnostic review, and fees are only earned on savings achieved. If the analysis shows no material opportunity, there is no charge.

The bottom line does not grow by itself. But for most retailers, the opportunity to improve it is closer than it looks.

Request a free payment cost diagnostic

EcomStream is an independent payment advisory firm based in Zeist, the Netherlands. We help retailers optimise payment costs and performance on a no-cure-no-pay basis, working exclusively for merchants, never for PSPs.