Most merchants treat checkout optimization as a payment problem. It is not, at least not entirely. The checkout process begins the moment a customer clicks "order" in the shopping cart, and for most of that journey, your PSP has no influence whatsoever.

Understanding where that boundary lies is worth real money.

Two distinct phases, two different objectives

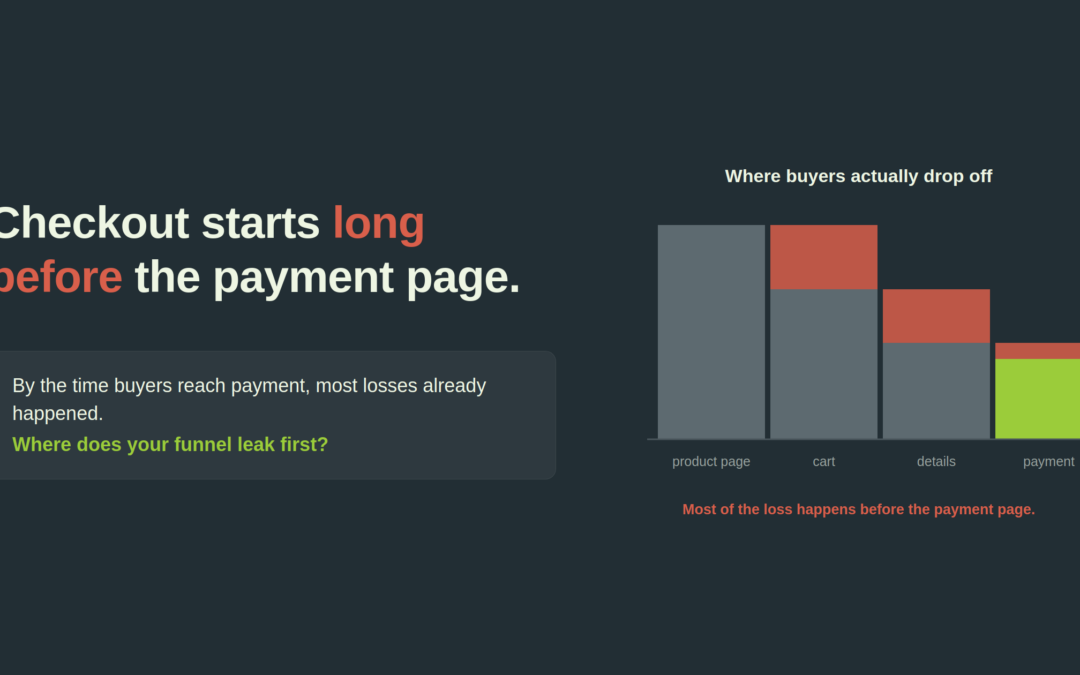

The online sales funnel splits cleanly into two parts. The shopping phase is about nurture: discovery, engagement, product information, and brand experience. Your customer is exploring. Speed is not the priority here.

The checkout phase is the opposite. Once your customer has made a choice, the only objective is to get them to payment confirmation as fast as possible. Every additional step, every moment of hesitation, every field that needs to be filled in is an opportunity to lose the sale. Your customer is not interested in the checkout process. They want to leave.

That distinction matters when you are allocating optimization effort. Most of the checkout, from the cart through address entry, login prompts, and delivery selection, falls entirely outside your payment provider's domain. Improving those steps requires work on your own platform, not a conversation with your PSP.

Where the PSP does have influence

Only in the final section of the checkout does your payment solution meaningfully affect conversion. That influence runs in two directions: before the payment is submitted, and after.

Before submission, the factors that drive conversion are mostly about relevance and experience. Offering the right mix of payment methods for each market segment matters more than offering the most. An English customer presented with iDEAL is a customer being asked to think, which is the last thing you want at this stage. The payment page should carry your brand's look and feel, even if you are redirecting to a hosted page. Tokenization and stored payment credentials reduce friction significantly on repeat purchases and eliminate the error rate on manually entered card numbers. On mobile, a responsive layout with numerical keyboard recognition is not a nice-to-have.

After the payment button is pressed, there are still failure points. Retrieval logic, the mechanism that offers an alternative payment method when an authorization fails without clearing the cart, directly protects conversion in a way that most merchants underestimate. Abandonment recovery via branded email is another lever that sits at the intersection of checkout and payment, and one that is often left unoptimized.

Authorization rate optimization deserves specific attention if you sell to markets outside Western Europe. In regions where card authorization success rates are structurally low, network optimization solutions offered by PSPs can recover a meaningful percentage of transactions. The commercial case for enabling these is usually straightforward.

Fraud management also lands here. If you sell fraud-sensitive products or services, the balance between conversion and fraud ratio is an active commercial decision, not a set-and-forget configuration. Overly aggressive fraud rules cost you legitimate revenue. Under-configured rules cost you through chargebacks and losses.

The practical takeaway

Paying in-store takes seconds. Online checkout still asks too much of the customer. The gap between a frictionless in-store experience and the average e-commerce checkout flow represents recoverable conversion. Some of that recovery happens on your own platform. Some of it happens in your PSP contract and configuration.

Knowing which is which, and acting on both, is where the commercial upside sits.

Want to know what your current payment setup is actually costing you? EcomStream offers a free diagnostic, no commitment, no cure no pay. Send an email to info@ecomstream.nl or call +31 (0)85 00 23 062.